Global LPG markets are spiraling into chaos as U.S.-China tariff battles reshape decades-old trading routes. American exports now bypass China, rerouting to Europe and Southeast Asia instead. OPEC+ cuts aren’t helping, squeezing supply further. Freight markets? Total mess. Spot terminal fees have skyrocketed while vessels waste time on longer routes. The industry’s efficiency is tanking. Market projections show a fragile balance through 2025—if you can call this madness “balanced” at all.

While the world once enjoyed relatively seamless LPG trading patterns, those days are firmly in the rearview mirror. The once-predictable flow of liquefied petroleum gas has splintered into a chaotic web of redirected shipments and inefficient routes. Thanks, trade war.

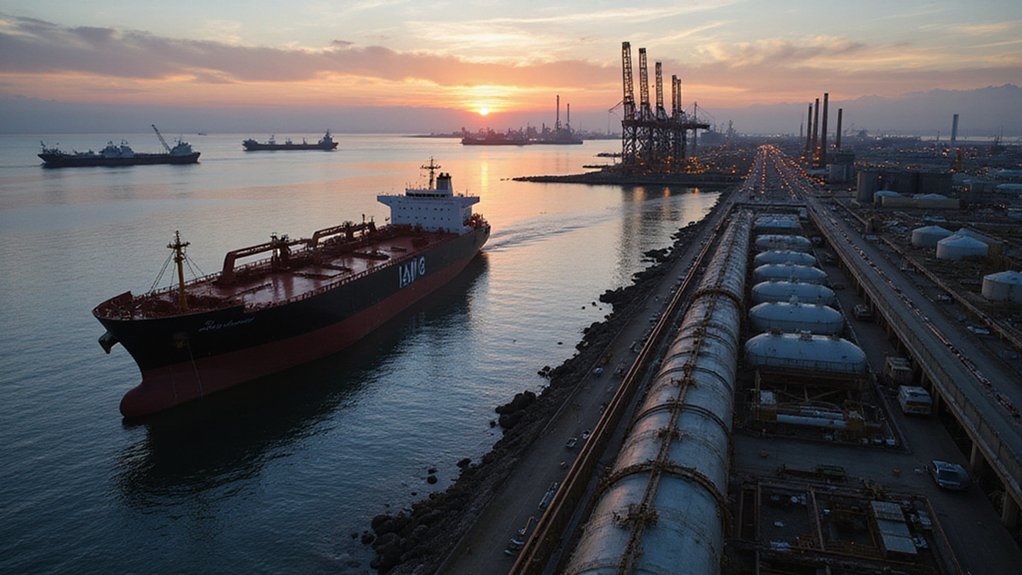

OPEC+ production cuts aren’t helping matters. With Middle Eastern output constrained and associated gas production limited, the global supply picture is tightening. Meanwhile, U.S. exports are surging—but guess where they’re not going? China. Those cargoes are now taking the scenic route to other Asian countries and Europe. With the return of President Trump back in January 2025, these trade tensions will continue to intensify.

OPEC+ cuts and Middle East constraints are forcing U.S. LPG shipments to bypass China for the long haul to alternative markets.

The freight market is having a complete meltdown trying to adapt. Spot terminal fees are through the roof, and shipping demand swings wildly from week to week. Vessels now face longer ballast legs and more repositioning. Not exactly the model of efficiency, is it?

China hasn’t stopped needing LPG, of course. They’ve just pivoted to other suppliers in the Middle East and Asia-Pacific. That’s created a domino effect across the entire market. Europe and Southeast Asia are now gobbling up America’s gas, creating entirely new trade lanes in the process. The halted Russian transit via Ukraine further complicates European gas supply security.

The impact on prices? EW spreads are widening dramatically. Market volatility is the new normal. And terminal capacity in the U.S. is becoming a serious bottleneck for global trade. Tight supply, robust demand—sounds like a recipe for price increases in 2025.

Asia remains the heavyweight champion of global LPG demand. Their petrochemical expansion continues unabated, putting pressure on olefins and LPG feedstock margins. Japan, South Korea, and India are all ramping up imports.

Looking ahead, supply growth is expected to gradually slow while demand keeps climbing. The global LPG market should maintain a fragile balance through 2025, with a projected CAGR of 3.66% through 2033.

One thing’s certain: the market fragmentation isn’t going anywhere. Get used to it.